Integration of External Financing Services in Banking - The Design and Validation of a Digital Finance Platform

This masters thesis demonstrates how banks can further develop their digital financial platforms to integrate external financing services, address their customers' needs, and enable new business models.

Topic

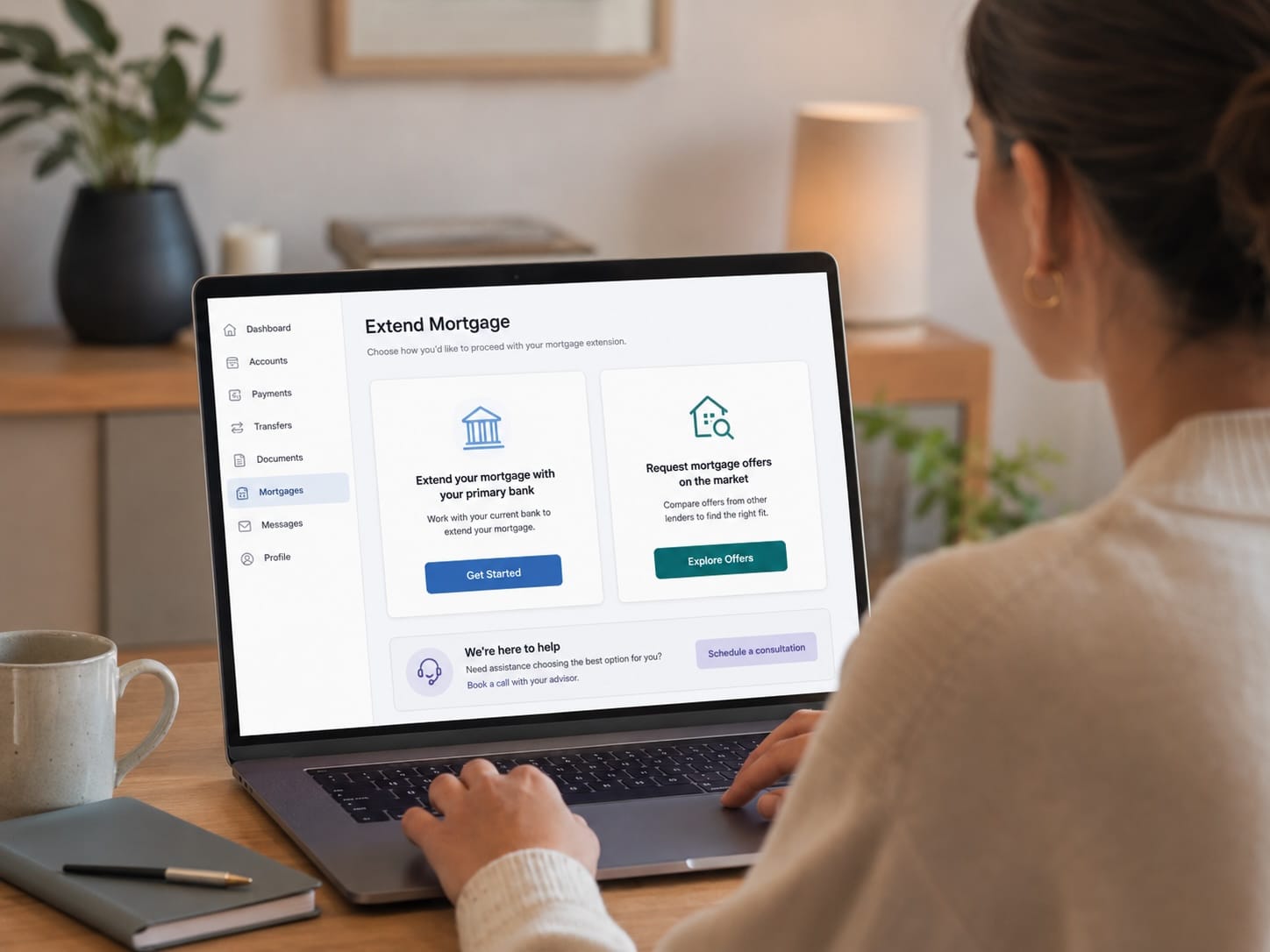

This master thesis examines how a bank’s digital financial platform should be designed to integrate external financing services and thereby enable new business models. The focus is on a conceptual mock-up that illustrates a customer journey for the digital extension of a mortgage via online banking. It demonstrates conceptually how customers could extend their existing mortgage with their primary bank or request alternative external financing offers. This illustrates how a bank can evolve from a pure product provider into a digital financial platform.

Relevance

This topic is relevant in practice because customers increasingly expect simple, transparent, and digital solutions in the financing sector. At the same time, open finance opens up new opportunities for banks to integrate external financial services into existing digital platforms. Integrating external financial services can help banks redefine their role in the digital financial ecosystem, secure customer touchpoints, and enable platform-based business models. In the mortgage business in particular, a guided digital customer journey can help strengthen trust, provide clarity, and boost confidence in decision-making.

Results

The results show that a digital financial platform creates the most value when external financial services are integrated into a guided customer journey in a controlled, transparent, and user-friendly manner. The mock-up illustrates that customers need guidance, trust, and confidence in their decision-making, especially when offers from external providers are integrated. At the same time, the study shows that such integration opens up strategic opportunities for banks to secure customer touchpoints and enable new business models through brokerage or platform approaches.

Implications for practitioners

- Implementation requires clear strategic positioning. Banks must decide whether they want to be primarily product providers, intermediaries, or platform orchestrators.

- Banks should integrate external financing services into a guided customer journey rather than presenting them as standalone offerings.

- External offers should be explained transparently, particularly regarding the provider’s role, data sharing, offer status, and the bank’s responsibility in the process.

- A digital financing platform should combine self-service with personal advice, particularly for complex or uncertain financing decisions.

- Banks should leverage controlled integration as a strategic opportunity to secure the customer interface, strengthen the primary banking relationship, and create new revenue opportunities through brokerage.

Methods

This master thesis follows the Design Science Research approach outlined by vom Brocke et al. (2020) and is based on the Three Cycle View proposed by Hevner (2007). The study combines a topic-driven literature review, four qualitative expert interviews, and an iterative design sprint with three evaluation rounds and a total of 18 interviews. The design sprint interviews were used for the iterative development and refinement of the mock-up, while the expert interviews contributed knowledge in the relevant thematic areas. Participants were purposefully selected to incorporate diverse professional and user-related perspectives. The evaluation followed the Gioia Methodology (Gioia et al., 2012).